If you think it’s time to buy a house, you need to answer two major questions: what are you looking for in a house? and how much can you afford to spend on a house?

You can answer these questions in any order, or go about answering them simultaneously. But deciding how much you can afford to spend first allows you to know if you can realistically afford the house that checks off the most boxes on your must-have list.

How Much House Can You Afford?

The Importance of Getting Prequalified

Whether you’ve been searching the MLS for months or even years, or you’re so early in your search that you don’t even know what the MLS is (it stands for Multiple Listing Service, by the way), finding your next home is exciting. And sometimes scary. But worse, perhaps, is that it can be heartbreaking if you find the house of your dreams only to realize you can’t afford it. So let’s start with cost. The point is not to scare you away from your dream house, but to make sure you make this major decision with your eyes wide open.

That’s why getting prequalified for a mortgage is so important. A prequalification from a lender will let you know exactly how much money the lender will allow you to borrow.

While the prequalification will tell you how much money you can spend, you still must decide what you’re comfortable spending – and there’s more to consider than just the purchase price of the house. You’ll also want to consider the upfront expense, the monthly payment, and ongoing costs because you still need to be able to afford food and utilities and other expenses.

Down Payment

Without a doubt, it can be difficult to save up the kind of money needed to make a substantial down payment. Traditionally, lenders require a 20% down payment. So if you’re looking at a $150,000 house, you’ll need to make a $30,000 down payment.

That said, you can find loans that do not require 20% down. In fact, depending on your credit score, you may be able to qualify for a loan that requires no down payment at all. You need to keep in mind, however, that any amount less than 20% down will likely require you to pay Private Mortgage Insurance (PMI) monthly to protect the lender in case you default on your loan. We’ll talk more about types of mortgages later.

Monthly Payment

Your monthly payment may consist of a number of things in addition to principal and interest (the borrowed amount required to pay back plus interest). As we just discussed, it may also include PMI if you do not put down 20%.

It will also likely include putting money into escrow to pay your property taxes. Putting money into escrow means breaking your estimated property tax total into 12 equal payments. Your lender puts that money into an account and pays your taxes when they are due.

The same principle is applied to your homeowner’s insurance. The premium is due once a year, but is broken down into 12 payments and your monthly payment goes into escrow until it is due. You are also going to pay for the first year in advance at closing.

And if your new neighborhood has a homeowner’s association (HOA), you likely will be charged an HOA fee, which will also be put into an escrow account monthly and paid once a year. Your HOA fees may range from a couple hundred dollars a year to several hundred dollars a month depending on the type of home you’re purchasing and the amenities included.

Closing Costs

When you go to sign the paperwork for your loan (called “closing”), you’ll likely have to bring money to pay for various fees (called “closing costs”) in addition to your down payment. Together the down payment and closing costs will be the total “money due at signing.”

Some of these closing costs include things like attorney’s fees, inspections, appraisals, a title search, a property survey, and, as we discussed earlier, the annual premium of your homeowner’s insurance. Many of these fees are split between the buyer and the seller.

According to Zillow.com, closing costs typically run 2% to 5% of the total purchase price of the home. A recent study indicated that the average buyer pays about $3,700 in closing fees.

It’s worth keeping in mind that sometimes the closing costs can be negotiated while making the offer on the house. If you’re in a buyer’s market, you may be able to get the seller to pay more than 50% of the closing costs. If you’re in a seller’s market, you may be asked to pay more than 50% of the closing costs.

Maintenance Expenses

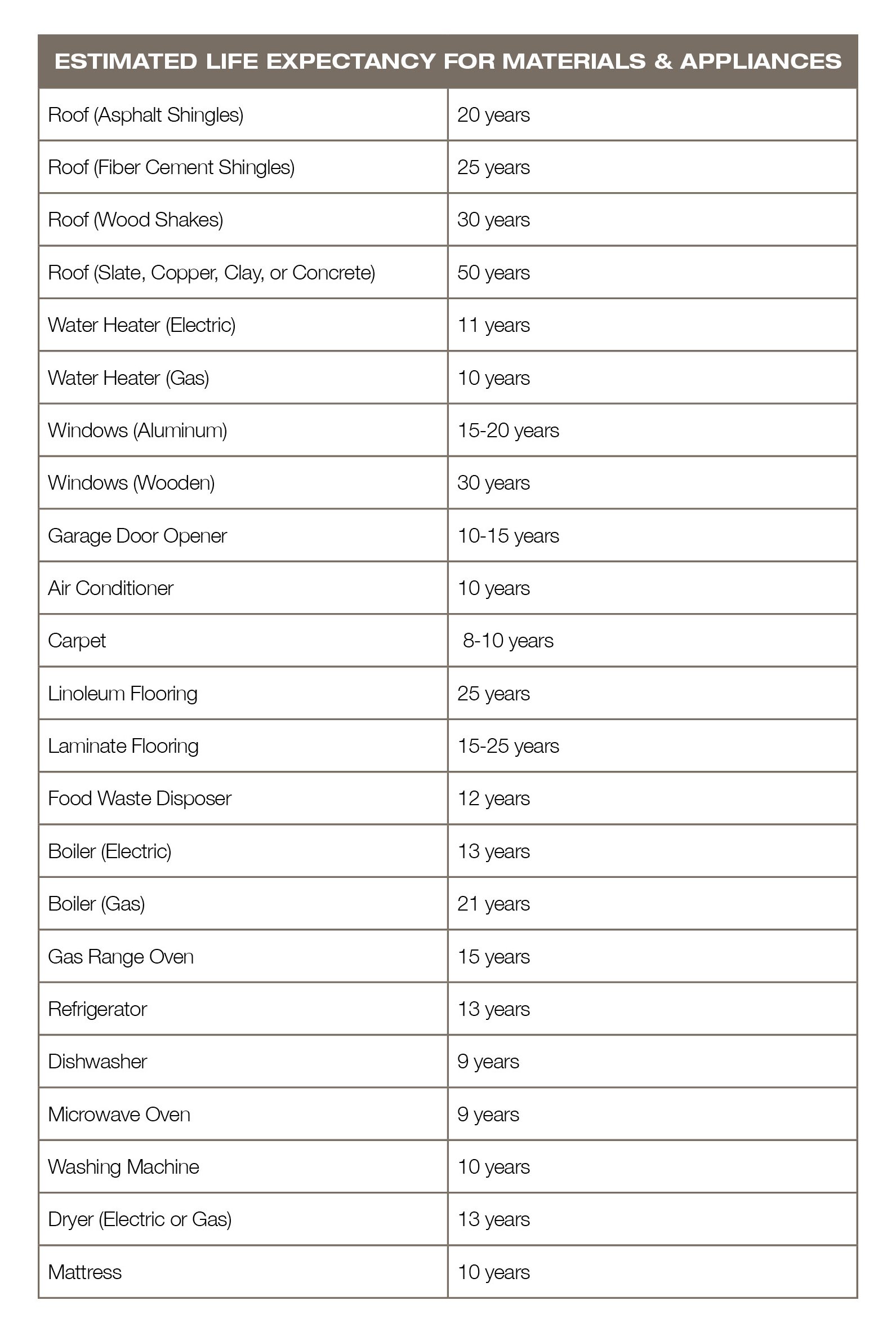

After it’s yours, you’ll face upkeep expenses on things like the roof, appliances, and the yard.

You may be wondering, just how long should various parts of my house last? Studies have been done that have provided these “rule of thumb” general estimates:

Based on the age of the house you’re buying, you may consider asking for a home warranty as part of your negotiations, even if the home inspection doesn’t raise any concerns. For instance, if the house you’re buying is between eight and 10 years old and hasn’t had any items replaced, you should be aware that any of the dishwasher, microwave, a gas water heater, air conditioner, carpet, and garage door opener may need to be replaced in the not-so-distant future. Purchasing (or negotiating) a home warranty (not to be confused with homeowner’s insurance) may help offset some expenses and give you some peace of mind.

And if you have a yard, you’ll want to think about the things you need for its upkeep, like a lawn mower, weed eater, hedge trimmer, fertilizer, and more.

Renting

You’ve probably heard people say that renting is essentially throwing money away because you aren’t generating any equity. You may even agree with that in general, but you may be concerned about the long-term commitment that buying a home requires. Maybe you aren’t sure how long you’ll live in your current town or city. Or maybe you don’t have enough in savings for a down payment. Perhaps your credit score isn’t as high as it needs to be.

So whether you’re renting by choice or out of necessity and want to buy a home someday, you’ll want to use the time wisely to try to grow your savings toward a down payment and build your credit. And of course while you’re doing that, you’ll have time to consider exactly what you want in a home.

So What Do You Do With All These Factors?

Talk to your mortgage loan officer. He or she will walk you through the information needed to determine exactly how much money you’ll be prequalified for. We’ll go into a lot more details about the mortgage process in the final section of this book. (Or you can skip straight there now.)

What Are You Looking for in a Home?

Now that we’ve talked about the factors that go into deciding just how much house you can (or want to) afford, we’ll take a look at the factors you’ll want to consider as you come up with your must-have list for your house.

What Kind of House Are You Looking for?

Are you looking for a single-family home in a neighborhood? Or a condo in the heart of the city?

If you’re single and wanting to enjoy all the city has to offer, a condo may be more your style. But if you have or want kids, you may be looking for a single-family home in a neighborhood close to parks and good schools.

Are you looking for a fixer upper? New construction? Somewhere in between?

Will this be your primary residence? Or are you looking for a vacation home? Perhaps a rental property?

Sorting through the answers to these questions will inform many of the other decisions you’ll have to make down the line.

Size

If you’ve already decided on a condo, you probably know that you’re looking at less square footage than if you’re wanting a single-family home. (That’s not always true, but often is.)

With a home, you’ll need to decide how big a house you’re looking for. How many bedrooms do you need now? What about in the future?

Do you plan to expand your family?

Or are your kids grown, and you’re hoping they’ll be returning soon for regular visits with your grandkids in tow?

Might your parents or in-laws need to move in in the not-so-distant future?

Some changes you can’t anticipate, but some things you certainly can factor in as you’re putting together your list of must-haves.

Location, Location, Location

If you’re wanting to be in the heart of the city, think about your favorite places to go: restaurants, bars, clubs. Do you want to be near major events, or maybe not so close that traffic and noise will be an issue? The important thing is to consider as much as possible so you can make a fully informed decision.

If you have young children, schools are probably important to you. You can find a letter grade for area schools online. But you can go beyond that and make an appointment and go visit the school in your desired neighborhood. These may help you whittle down the neighborhoods you’re seriously considering. You may not be thinking of selling at the moment, but schools can help your resale value too.

How far are you willing to be away from the places you go?

Is it important that your commute to work each day be just a few minutes? Or are you willing to drive a bit to get more house or to be zoned for a particular school?

How close do you want to be to your favorite restaurants and shops?

Do you want a quiet neighborhood or a street where kids roam up and down, playing with their friends?

No one can answer these questions for you. And each decision may require a tradeoff on another factor. A real estate agent can help you understand the tradeoffs you’ll have to make in your particular town or city.

Yard

Do you want a yard? Maybe you’ve always dreamed of growing your own vegetables and herbs in the backyard. Maybe your idea of the perfect house includes a wooded lot and lots of flowers. Maybe you just can’t wait to play tag football on the lawn with the extended family on Thanksgiving.

No matter what your dream, you’ll want to think about how big a yard you want and how much time, energy, and/or expense you’re willing to take on for its upkeep. Like we discussed in the maintenance section above, a yard may require equipment and other supplies like a lawn mower, weed eater, hedge trimmer, fertilizer, and more.

Again, the important thing is to consider what you want and be realistic about what it entails. The last thing you want is to wish you’d remembered how much you’d always wanted a yard when you bought a condo or townhouse – or that you wish you’d considered how much time it was going to take to mow your two-acre lot.

Amenities

Many newer neighborhoods offer attractive amenities like neighborhood pools, tennis courts, hiking trails, playgrounds, and more. Some planned communities even have schools and grocery stores within them.

Condominiums are also likely to offer amenities such as pools, fitness centers, and parking garages.

You’ll likely have to pay HOA fees to help pay the upkeep on these community features.

The Search

Real Estate Agent

We briefly mentioned a real estate agent earlier, but we’d be remiss if we didn’t discuss the advantages of having a real estate agent.

He or she can help you talk through your wish list, then help schedule appointments to see homes that might be good fits. Your agent will

serve as a go-between for you and the seller (or seller’s agent) with any questions you might have and ultimately help you negotiate the best deal possible and work with you through the closing process.by your side. Having a professional help walk you through the home-buying process can make your search a lot less stressful (and who couldn’t use less stress?). A good agent represents your interests – not anyone else’s.

The Hunt

Now that you’ve considered all the things you’re looking for in your new house, let’s think about the questions to ask when you’re wondering if this house could be your house.

Be prepared to look at a lot of homes – both online and in-person. It may take days, weeks, or months – depending on your criteria and the number of homes available in your area.

You’ll want to pay special attention to two things: the condition of the house and the feel of the area.

The House

Many of these will be addressed by an inspection you’d have done after an offer was accepted, but pay attention to the following:

- The foundation – Look for cracks and any other damage. Look to see if the floors have any spots that are lower or higher than the rest.

- The doors – Check to see how the doors open and shut. In an older home, doors that rub when opening or won’t shut are indicators that the house has settled. In a newer home, though, those may be signs of poor construction.

- The attic – Look to see if the roof framing is braced properly. Look for a sag in the rafters.

- The furnace – Ask how old the furnace is. An older one is a risk, but it’s impossible to know how long it will last. They are expensive to replace, but the newer models are far more efficient.

- Termite damage and signs of mold – Most houses built before 1950 will have some form of termite damage, but you’re looking for active infestations. Mold can make the house unhealthy.

- The wiring – Ask your inspector if the wiring has been updated if you’re looking at an older home.

- The roof – Ask how old it is, and look for weather damage.

- Insulation – Are the windows, walls, and doors insulated?

A concern with any of these isn’t necessarily a deal-breaker, but you should consider all these factors (plus anything you’re concerned about or that your inspector raises). Some of these problems may require expensive fixes, and too many may signal that the house will be expensive to maintain. However, it’s possible you can address issues during the negotiation phase, and the seller will agree to repair something or give you a financial concession since you may have to pay to address an issue.

The Feel of the Area

In addition to geographic location and school zones, you’ll also want to consider the feel of the area.

Talk to people who live in the neighborhood. Visit open houses and ask questions. Do you see people out walking their dogs? Are there kids riding their bikes or tossing a ball around? Are people taking care of their homes? Get a sense of what it would be like to live there day in, day out.

Find out what you can about services like trash pickup and road maintenance.

Making an Offer

You’ve found it. The house you want to buy. The house you can see yourself living in. So now what?

It’s time to make an offer. Gulp.

It’s a good idea to know what other homes of comparable size and condition in the area have sold for recently. (Your real estate agent will probably do this, if you have one.) That will give you an idea of the property’s market value.

Make an offer to the seller (usually through their agent). Your offer will, of course, include a price, but it may also include other requests like leaving the refrigerator or the washer and dryer. (Like we mentioned earlier, being prequalified for a mortgage is a big deal for you. It’s also a big deal for your seller: they’ll be glad to know that you already have financing lined up and are more likely to close. This is especially important if you are in a competitive market.)

Remember: this is a negotiation, and everything is negotiable. Don’t be surprised if they counter-offer. And be prepared to walk away if it’s not the right deal for you. It may be disappointing, but sometimes it just isn’t meant to be.

Once you and the seller have agreed to an offer or counter-offer (or counter-counter-offer), you’re “under contract.” Congrats!

From Contract to Closing

Now that you’re under contract, a number of things will need to be done before you close and the house is yours. It’s likely that someone from your real estate agent’s office (or the seller’s) will coordinate with the lender to set up these steps. But just in case, here are a few things you’ll need to make sure get done.

An inspection. You’ll likely want an inspection to make sure there aren’t major flaws in the house that you can’t see. Your inspection report will detail a number of things. It may raise questions about the age of the air conditioner or the condition of the roof. It may raise less significant issues like the door to the shower doesn’t close properly. Like we mentioned before, after you get the report, you may enter another phase of negotiations with the seller to ask them to address any concerns you have.

An appraisal. Your lender will order an appraisal. This will give the lender confidence that the house is actually worth what you’re borrowing to pay for it. (Talk with your real estate agent about a contingency clause based on an appraisal before you submit an offer.) If the appraisal is lower than your offer, you may have to bring more cash to closing than you originally intended – or the seller may agree to sell the house at the appraised value. Remember that you can always get a second opinion on the appraisal (though you have to be willing to pay for it).

Homeowner’s insurance. You’ll need to purchase homeowner’s insurance. Don’t wait too late in the process because the underwriting process could delay your closing if it takes longer than you expect.

Applying for a Mortgage

Getting Prequalified

Like we mentioned in passing already, getting prequalified for your loan is important. Not only will it tell you how much house you can afford, it’ll also tell a potential seller that you already have financing lined up.

To get the prequalified process going, your lender will ask you for several documents for each person whose name is on the loan:

- Birthdates

- Social Security Numbers

- Copies of driver’s licenses

- Copies of at least two most recent pay stubs

- Copies of W-2 forms

- Two-year residence history

- Statements from your financial institution for the last two to three months

- Copies of tax returns for the last two years (for self-employed borrowers or those with rental properties)

- Copy of divorce decree/property settlement, if applicable

Interest Rates

Many types of mortgages exist in the mortgage market. The one that’s right for you will depend on your goals and your specific financial situation.

First, you’ll explore whether you need a fixed rate or a variable rate. Fixed-rate mortgages (also known as conventional loans) are what the name implies: loans with a constant interest rate for the length of the loan (usually 15 or 30 years). This is likely what you’ll want if you plan to stay in the home for many years. That’s because the assumption is that interest rates will increase over time, and a fixed rate makes budgeting more predictable. Generally speaking, the longer the term of the mortgage, the higher the interest rate will be.

Variable rate mortgages (also called adjustable rate mortgages, or ARMs) begin at a lower rate for a short period of time and then adjust at set times (how many, or how often, would depend on the specifics of your mortgage) to the market rate at the time (it could be lower; it could be higher). Variable rates are popular for those who plan to move within just a few years because they are able to take advantage of the lower rate before selling before the rates adjusts upward. Another popular practice is to refinance to a fixed rate before the rate adjusts.

Mortgage Types

Beyond fixed-rate loans and variable-rate loans, additional mortgages are available:

VA loans. Veteran Affairs loans are offered by private lenders such as credit unions and banks. A portion of the loan is guaranteed by the U.S. Department of Veteran Affairs. They are designed for veterans, service members, and eligible surviving spouses.

VA loans are available with up to 100% financing (of the purchase price) available, meaning no down payment is necessary in some cases.

FHA loans. Backed by the Federal Housing Administration (FHA), FHA loans have helped people who may not qualify for a traditional mortgage since 1934. An FHA loan is issued through traditional lenders and insured by the FHA.

FHA loans are available with down payments as low as 3.5%.

USDA loans. Backed by the Department of Agriculture’s Rural Development Housing and Community Facilities Programs, USDA loans are offered by approved lenders and are intended to help people with low to moderate income buy a house in eligible rural areas. Click here to find out if you’re eligible for a USDA loan.

Closing

It’s time to make that house yours. After you close on the purchase of the home, it’ll be yours. You’ll sign a lot of papers. You and the seller may close at the same time, or they may be done at different times. It just depends. At the very least, your real estate agent and an attorney will be there to walk you through the process.

You’ll need to bring several things to the closing (or have them sent ahead of time):

- Proof of homeowner’s insurance

- A certified or cashier’s check for your down payment and your closing costs

- A copy of your contract

- Unexpired government-issued ID (for borrower and co-borrower)

- Anything your lender requires to close the loan

It’s an exciting time, and it can be stressful too. Be willing to ask questions about what it is you’re signing. Try not to worry too much if something doesn’t go as planned. Maybe someone’s late. Maybe the seller hasn’t quite gotten all their stuff out of the house. Remember: at this point, everyone wants the sale to go through, and soon enough, you’ll have keys to your new home in hand.

And that’s what makes all the effort worthwhile.